At the beginning of July 2024, the UK experienced a change in government for the first time in 14 years following the general election, which resulted in a landslide Labour win. Throughout the election campaign, Labour were continuously challenged on the topic of taxation, leading to them ruling out increases in Income Tax, National Insurance, and VAT.

The new government has firmly committed to adhere to its own fiscal rules, which includes only borrowing money for investment purposes. The announcement of a £22bn black hole in public finances, combined with restricted borrowing headroom and the commitments to not increase certain taxes, has fuelled speculation as to which taxes might be increased in upcoming budgets.

Speculation has intensified since recent comments by the Chancellor, Rachel Reeves, indicated that tax increases are probable and Prime Minister Keir Starmer warned that the budget will be “painful”.

One such tax which has been mooted for change is Capital Gains Tax (“CGT”). CGT is a tax on the profit arising from the disposal of an asset. When a business owner sells their shares in a business, the gain on these shares is usually subject to CGT.

How might CGT change in upcoming budgets?

Alignment of CGT rates with Income Tax

The government may decide to align the rate of CGT (20%) with Income Tax (45%). The Government’s likely motivation for this – beyond balancing the books – is that CGT was paid by c.1% of taxpayers in 2022-23 and can be seen as a wealth tax rather than a tax on workers.

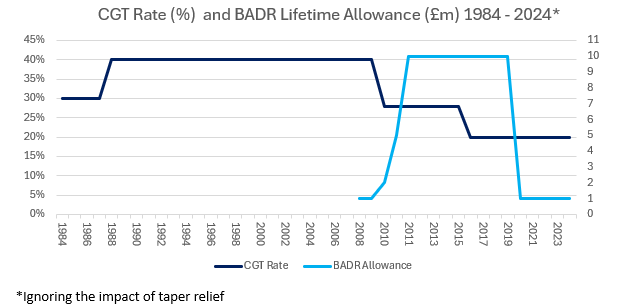

The alignment of CGT and Income Tax rates is not unprecedented; between 1988 and 2008, the rate of CGT was 40%, equal to the top rate of income tax during this period.

On the flip side, aligning the rates of CGT with Income Tax is not guaranteed to close the deficit; historically, increased rates of CGT have yielded lower returns for the exchequer as they can lead to people accelerating disposals ahead of a change or simply retaining assets and undertaking tax planning.

Our expert tax teams can assist in navigating the CGT landscape and advise on strategic planning to minimise liabilities.

Abolition of Business Asset Disposal Relief (“BADR”)

Business Asset Disposal Relief, previously known as “Entrepreneurs Relief”, is available to qualifying shareholders and allows for a lower rate of CGT at 10% to be applied to the first £1m of lifetime gains when selling shares in a qualifying business.

To qualify, the following must apply for at least 2 years up to the date you sell your shares:

- You are an employee or office holder of the company (or one in the same group).

- The company’s main activities are in trading (rather than non-trading activities like investment) – or it is the holding company of a trading group.

- You hold at least 5% of the shares and voting rights

A potential change to CGT may be to abolish BADR, ensuring that all capital gains are taxed at the same rate. BADR has already come under attack when the lifetime limit was reduced from £10m to £1m in 2020.

What does this mean for business owners?

Potentially higher tax on business sales

An alignment of CGT with Income Tax could mean that business owners pay 25% more tax on the sale of shares in a business. In monetary terms, the sale of shares in a business for £10m would attract £2.5m additional tax. To achieve the same proceeds, net of tax, a business would need to be sold for £14.5m (a 45% increase).

Similarly, the abolition of BADR would remove £100k of relief currently available to qualifying shareholders.

Valuation gaps

If there is an increased tax on the sale of shares, business owners’ valuation expectations may increase to be able to achieve the desired outcome from a sale in terms of net cash. This could create a gap in valuation expectations between sellers and buyers, which can make completing a sale more difficult.

Working with a professional adviser, such as PKF Smith Cooper’s Corporate Finance team, can help maximise the value of your business before the sale process commences, provide access to hard to find buyers and create a competitive process to drive higher business valuations and achieve outcomes that meet your objectives.

Thoughtful planning required

An increase in CGT is not guaranteed, the Government may seek to protect entrepreneurs or retirement sellers, and the timing of an increase, if there is to be one, is unknown. The next budget is set for 30th October 2024, which will be followed by a spring budget in March 2025.

It is crucially important for business owners to consider their options now; delaying a business sale could prove costly. Entering a sale process in the near future could mitigate the risk that is derived from the ever-looming threat of an increase in CGT rates and an abolition of BADR.

It is important to ensure however that a business sale is not rushed, and that a process is embarked upon for the correct reasons and at an appropriate time. PKFSC Corporate Finance work with business owners to create bespoke exit strategies to meet objectives.

Need help selling your business?

Whether you choose to wait or push forward with a sale, we can ensure your business is prepared and optimally positioned to maximise its sale value.

At PKF Smith Cooper, our Corporate Finance team has broad experience of offering tailored advice to our clients and forming strategic approaches to potential disposals.

Contact us to find out more about how we can help.