The waste industry in the United Kingdom is undergoing significant transformation, driven by environmental legislation, technological innovation, and evolving consumer and business behaviours.

The waste industry encompasses the collection, transport, processing, recycling, or disposal of waste materials. The UK market, valued at several billion pounds, is a vital component of the nation’s sustainability agenda, supporting the transition towards a circular economy and net-zero carbon emissions.

In this sector insight report, our Corporate Finance team provides an overview of the waste management industry in the UK along with a summary of the M&A activity in the market during 2025.

Market overview

Rising environmental concern drives people and businesses to recycle more, boosting demand for recycled waste collection

Overview

The Non-Hazardous Waste Collection industry has adapted well to surging demand for recycling from commercial, industrial and residential clients.

Government recycling policies are elevating sustainability. Initiatives to push recycling and waste treatment have boosted demand for waste collection and recycling services, bringing in more revenue.

Government policies have led to waste treatment being on the rise. Elevated environmental consciousness has brought on cleaner and stricter waste processes.

Rising public concern over the environment has intensified pressure on consumers and businesses alike to limit the amount of waste sent to landfill sites and recycle more, directly boosting demand for waste collectors.

Household waste is on the rise. This is due to more people shifting permanently to working from home, so they are producing more household waste.

Increased sustainability initiatives and waste treatment requirements will provide the industry with opportunities for revenue growth. The industry is expected to grow at a compound annual rate of 6.8% through to 2029-30 providing an industry valuation of c.£17.3 billion in the UK.

While revenue growth is expected, profit margins are widely expected to be squeezed as a result of sustained high fuel costs, increased staff expenses arising from recent budget announcements, and rising Landfill Tax associated with increasingly stringent sustainability policies.

It is expected that deal volumes may increase as business owners look to exit the industry and realise their value, although transaction volumes have been steadying in recent years.

We expect further consolidation to happen with the consolidators making further acquisitions to benefit from additional economies of scale and to bring in specialist circular economy capabilities.

Industry M&A activity in the UK

Consolidation continues with consolidators acquiring many assets as they compete for market share and expertise

Overview

M&A activity in the market is driven by three types of buyers:

- The original consolidators who already have mature strategies of acquiring small players to bolster business critical areas, whether this be due to geographical presence or technical expertise

- Secondly, new consolidators to the market, focusing on smaller geographical areas and building scale, or acquiring complementary specialisms to increase their modest operations compared to the large consolidators

- Thirdly, and most recently, there has been a significant increase in interest from private equity buy and build specialists acquiring platform investments and creating strategic acquisition plans within the waste industry

Many major consolidators including Biffa (Energy Capital Partners), Viridor (KKR & Co), Reconomy Group (EMK Capital) and Enva Group (Squared Capital) have all received investment from private equity and used funding to continue their consolidation journeys.

The increase in private equity investment is due to the increased impetus on sustainable and green waste management solutions providing a strong outlook for the market in the future.

As well as a strong industry outlook, the industry already benefits from largely recurring revenue streams that are resistant to both economic and epidemic issues, showcasing it as an essential sector for investment for strong returns and downturn risk management.

Deal focus

A selection of deals completed in the UK waste industry during 2025

Overview

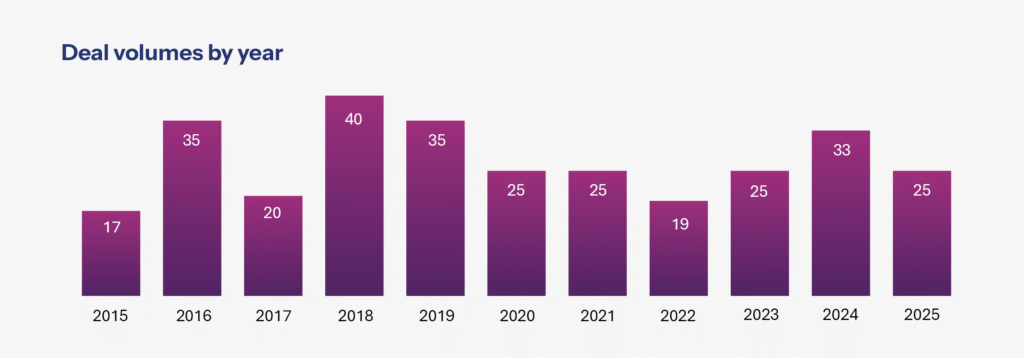

Transaction levels in 2025 were moderate overall and largely consistent with the past five years, with growing investor interest in niche businesses.

Whilst many acquisitions are being completed by those within the waste industry already, the continued focus on the circular economy is continuing to drive interest from companies within adjacent industries due to increased reporting responsibilities relating to waste and recycling.

Building materials businesses, such as Heidelberg Materials, have invested in construction waste and aggregates recycling centres to increase their product offering to include recycled materials in concrete, aggregates and asphalt for customers and projects of all types and applications.

The key transaction of note in 2025 is Macquarie’s acquisition of Renewi Plc, a deal showing further investment into waste and recycling for Macquarie, alongside its investment in Beauparc, a serial acquirer within the space.

First Mile, which was recently acquired by US private equity firm Warren Equity Partners, continued its acquisition drive, completing two acquisitions (Greenzone and Albion Waste) in Q1 of 2025; these acquisitions added significant scale to First Mile’s national and London capabilities.

Activity shows there is M&A appetite for both increases in geographical presence from new consolidators in the market, whilst other acquirers are looking for niche specialisms to increase capabilities.

Infrastructure funds and UK waste

Growing interest from infrastructure investors in the UK waste management sector

Guest contributor – Nap Ghag

Nap Ghag is the Founder and Managing Partner of Mulberry Advisors, an independent corporate finance advisory firm serving investors, owners and managers of SMEs.

Nap has over 20 years’ experience in professional advisory, providing specialist expertise in waste, recycling and infrastructure. He has advised on transactions involving many of the largest operators along with privately owned SMEs within the waste sector. Nap was formerly head of corporate development at Ward Recycling, delivering transactions within a total waste management business.

His career includes long-standing positions at Deloitte and KPMG, where he specialised in corporate finance infrastructure advisory. Through this experience, he has cultivated extensive relationships with infrastructure investors, including those actively considering the waste sector.

Overview

Infrastructure funds have shown a clear and sustained increase in investment in UK waste businesses, establishing the sector as a core sub-theme of UK infrastructure and mid-market M&A activity over the past five years.

Why infrastructure funds are investing in waste

- Waste management is a non-discretionary service driven by population growth and economic activity rather than consumer spending. Service continuity is critical to public health, environmental protection and regulatory compliance, positioning waste as essential infrastructure rather than a purely industrial service

- Infrastructure investors are well versed in operating within highly regulated environments, such as utilities, transport and energy, and are therefore comfortable underwriting the regulatory complexity of the waste sector. Assets with environmental permits, long-term contracts and essential service characteristics are increasingly viewed as utility-like, aligning well with infrastructure risk-return profiles

- High upfront capital requirements, regulatory barriers to entry and long asset lives suit infrastructure funds deploying patient capital with long-term investment horizons. Many waste assets benefit from long-term contracts, indexed pricing and local authority relationships, supporting predictable, inflation-protected cash flows and income stability

- In addition, infrastructure investors face increasing pressure to deploy capital into assets with clear ESG outcomes. Waste delivers measurable environmental benefits while retaining strong commercial fundamentals, supporting long-term demand visibility and attractive risk-adjusted returns. Compared with more mature infrastructure sectors such as water and energy, waste offers higher return potential alongside essential service characteristics, continued consolidation opportunities and regulatory growth drivers, sustaining investor appetite without a proportionate increase in risk.

Industry M&A trends in the UK

M&A appetite has clearly shifted from traditional landfill, general collection and hazardous waste to more investable niches

Overview

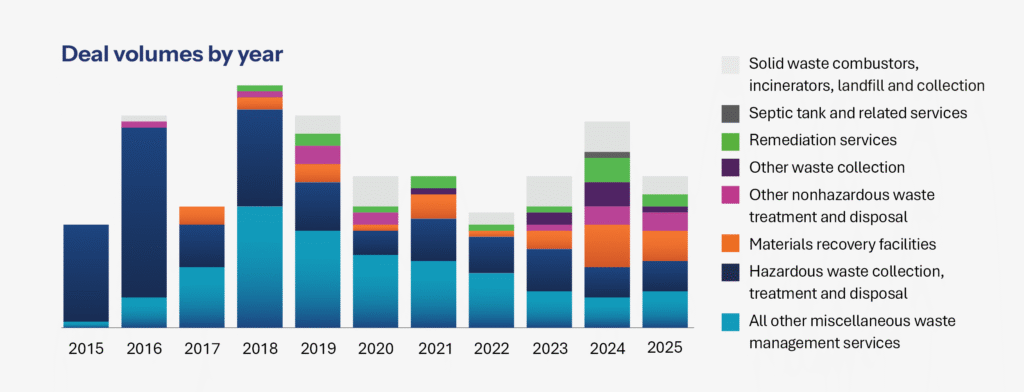

Since 2018/19, there has been a shift towards a more diversified M&A waste market, where deals are showing increased activity in more niche subsectors, indicated by the more diversified split in the latter years of the graph below.

The emergence and increased activity of the subsector “Materials Recovery Facilities”, which involves deals mostly relating to metal and battery recycling, is one of the sub-sectors on the rise.

Waste Electrical and Electronic Equipment (WEEE) and battery recycling deals are almost absent before 2018, but from then onwards, there has been a clear uptick in both deal count and investor interest. Additionally, an analysis of deals completed in the EU over the past 10 years, showed growth in volumes, and a clear upwards trend in Waste-to-Energy deals, implying further that acquirers are increasingly looking for investable niches.

We expect this was driven by the Circular Economy Package (EU,2018) and the UK’s Resource and Waste Strategy (2018) which set ambitious recycling and landfill diversion targets (e.g. 65% municipal recycling by 2035, maximum 10% landfill).

Additionally, the Extended Producer Responsibility (EPR) for packaging, WEEE, and batteries (phased in from 2019-2025) created new investable niches in materials recovery, electronics recycling, and organics. The Plastic Packaging Tax (2022) further incentivised investment in plastics, Materials Recovery Facilities (MRFs), and closed loop recycling.

M&A activity from the UK’s top 10 acquirors

Active acquirors are showing more interest in niche segments that have new offerings and technologies to complement their previous geographical expansions

Overview

In addition to the industry M&A trends outlined previously, the slowing of the deals in the Hazardous Waste and Miscellaneous Waste sub sector can also be attributed to the consolidation of the traditional waste management methods by the largest players in the industry.

In the UK, the top 10 acquirers have seen a reduction in deal numbers in recent years, as shown in the chart below.

The waste industry in the UK is at a pivotal point, balancing regulatory compliance, environmental stewardship, and economic pressures which have all led to a steadying of M&A activity.

Businesses that invest in advanced technologies, embrace circular business models, and collaborate across the value chain will be best placed to thrive in the evolving market landscape of the waste industry.

As a result, the change in M&A activity is likely to focus moving away from geographical expansion, which has been the driver for the last decade, to more niche circular economy offerings with new methods and technologies, as the largest players look to cement future opportunities through increased capabilities.

Market drivers

Increased public environmental concern twinned with increases in legislation is pushing industry players to circular economy opportunities

Public concern over environmental issues

Increased public awareness and greater environmental consciousness among consumers and businesses is increasing demand for sustainable waste solutions.

This chart demonstrates the increase in public concern over environmental issues throughout the 21st century. Public concern is expected to continue to grow, growth can be attributed to greater understanding of environmental issues and the concern over global warming.

The UK’s target to achieve net zero greenhouse gas emissions by 2050 is promoting investment in advanced waste processing technologies, energy-from-waste (EfW) facilities, and circular economy initiatives.

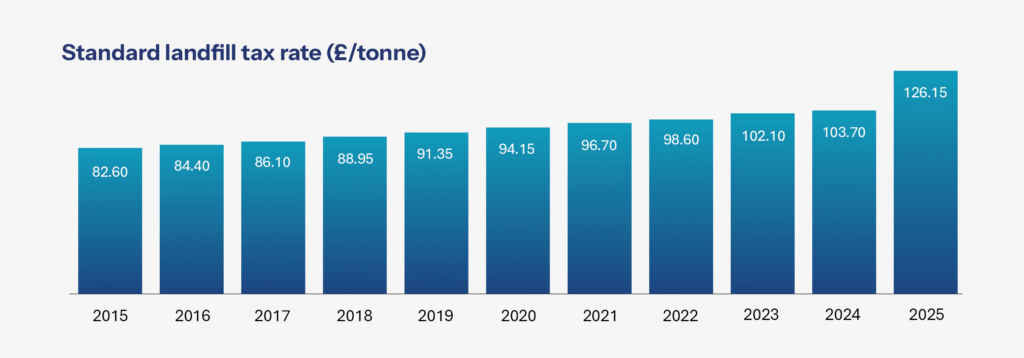

Standard landfill tax rate (£/tonne)

Stringent legislation, including UK and EU directives, such as the Waste Framework Directive and the Landfill Tax escalator, has spurred increased recycling rates and reduced landfill dependency.

The Landfill Tax Escalator (rising from £48/tonne in 2010 to £126.15/tonne by 2025, a significant 22% increase from 2024) and the Landfill Allowance Trading Scheme (LATS, until 2023), incentivised the diversion of hazardous and difficult waste from Landfill, driving increased M&A activity and appetite for specialist waste treatment and disposal businesses.

Unlocking the potential of UK waste management

We recently held an industry roundtable discussing how to unlock the potential of UK waste management

Overview

The UK waste management sector is expected to grow by nearly £4 billion over the next five years, driven by a variety of factors such as environmental pressures and population growth. However, the sector faces many challenges that require improvement, and complex regulations, strained local budgets and fierce competition for investment threaten its projected progress. What steps can be taken to unlock the sector’s full potential?

Current problems in the sector

One of the primary challenges is the rise in public confusion around recycling. Consumers are often confused about what can and cannot be recycled, and many businesses struggle to fully understand new waste regulations.

The term ‘waste management’ has also become outdated in recent years and no longer reflects the sector’s evolving role in sustainability, with ‘resource recovery’, ‘urban mining’ or ‘commodity management’ being preferred terms for what the sector has to offer.

Furthermore, the waste sector is moving towards circular economy models, adapting from linear disposals to circular systems that reuse, repair and repurpose materials. With private equity and institutional investors focusing heavily on ESG performance, this shift in economy model aligns directly with investment criteria as well as government sustainability goals.

Growth opportunities

Waste management is essential to a functioning society and includes a wide range of services, not just recycling. Waste is no longer waste but instead considered as ‘resource recovery’.

This understanding of how the waste sector is being shaped is crucial to its future growth opportunities, particularly in the public’s perception. An improved clear and accessible messaging, especially around food waste and plastic film recycling, is essential to unlocking compliance and growth.

A reframing of waste management emphasises the economic and environmental value of materials that can now be seen as reused, repaired or repurposed rather than waste. As an example, Innovate Recycle, based in Coventry, has invested in a larger plant to deconstruct end-of-life carpets, reclaiming materials such as polypropylene and calcium carbonate, and returning them to UK manufacturers for use in products like medical-grade equipment.

Alongside sector growth opportunities, waste management faces increasing interest in prospective buyers, with ESG performance attracting many private equity investment opportunities. Traditional waste management no longer appeals to private equity investors, and instead, investors are shifting their attention to innovations that are supporting the circular economy.

Market outlook

Growth is supported by regulatory requirements, investment in infrastructure, and societal shifts towards sustainability

Overview

The UK waste management industry is expected to experience growth, supported by regulatory requirements, investment in infrastructure, and societal shifts towards sustainability. Recycling and resource recovery will remain key areas of focus, with policy frameworks incentivising innovation and the adoption of circular economy principles.

Legislative changes

The Simpler Recycling Regulation was introduced on the 31st March 2025. It requires businesses with 10 employees or more to separate glass, paper, metal, cardboard, plastic and food waste. This policy will extend to smaller businesses in March 2027.

Mandatory separate food waste collection means new investment into anaerobic digestion plants and composting facilities may be required.

Household Waste Separation regulation is set to be introduced in March 2026 which requires waste to be separated into four categories:

- Food and garden waste

- Paper and card

- Dry recycling

- Residual waste

Initiatives such as Extended Producer Responsibility (EPR) schemes are set to shift more of the cost and responsibility for waste management onto manufacturers, which may result in a shift of focus and opportunities for well advanced circular economy businesses.

The Digital Waste Tracking System (DWTS) will become mandatory for waste receiving sites and all other regulated operators from October 2026 and April 2027, respectively. It is a centralised system designed to modernise how waste is recorded, monitored, and reported across the UK. This system aims to provide accurate data to support the UK’s goals of eliminating avoidable waste by 2050.

Companies that are already using waste management software and IoT sensors that can be integrated into the DWTS will avoid costly last minute compliance upgrades, minimise risks of fines/reputational damage and offer predictable compliance.

Market consolidation may continue, with mergers and acquisitions creating larger, more efficient operators. Digital transformation will further streamline logistics, reporting, and compliance. However, the sector will need to address ongoing challenge around contamination to realise its full potential.

There is increasing emphasis on designing out waste, reusing materials, and developing closed-loop systems leading to increased circular economy business models.

The emergence of new technologies and innovations in chemical recycling, biowaste processing, and artificial intelligence are enabling higher recovery rates and more efficient operations.

This increased emphasis on separation brings into question companies with digital waste tracking systems and recycling technology, where we may expect acquisitions of software providers and recycling technology firms (e.g. AI sorting or IoT sensors) alongside traditional haulers.

Simpler recycling regulation means that businesses will have to collect the same set of recycling materials, which smaller waste management firms may struggle with if there is requirement to invest in extra bins, trucks and sorting facilities. A higher valuation may be applied to companies that can already have the infrastructure in place to manage these new rules.

Businesses operating in the waste industry must undergo decarbonisation of their own operations; this could include fleet electrification, renewable energy use, and methane capture to reduce the carbon footprint of waste management activities.

Finally, the UK waste sector has clearly shifted from traditional landfill, general collection and hazardous waste to more investable niches, particularly WEEE, battery recycling, WtE, advanced plastics recycling and circular economy models.

Next steps

Set up an initial meeting and discuss the right option for you and your business. Before the meeting it is helpful to consider the following topics:

- What are your objectives? Are you looking to exit or grow your business to the next level?

- Would you like to remain involved going forward? What is your desired timeline for exit/growth?

- What legacy do you want to create for the business and its employees?

- How has your business performed historically, and how robust are your financial systems and revenue contracts?

- What are the skill sets and ambitions of your current management team/family members working within the business?

- What are your plans for growth, and what does your business need to deliver this?