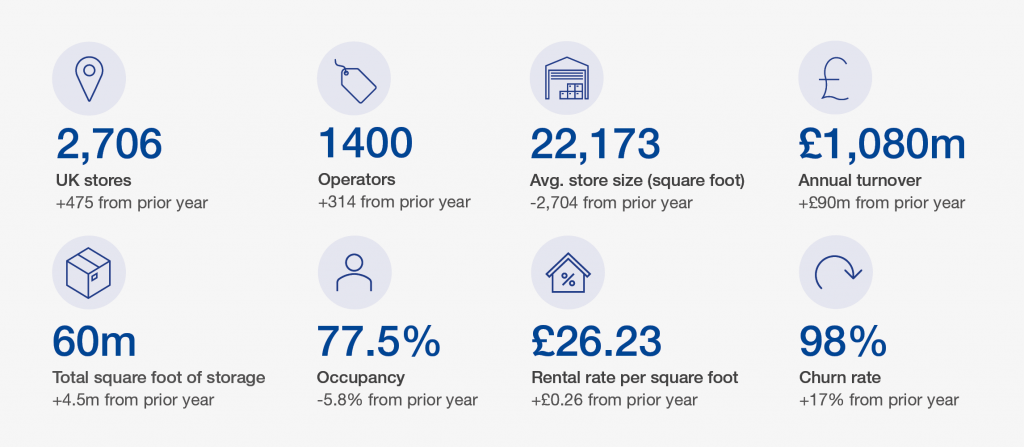

The self-storage sector in the UK has continued to expand, reaching a new industry milestone for revenues as it surpassed £1b per annum. 475 new stores and 4.5m sq. ft. of additional self-storage were also created.

Market overview

The self-storage sector in the UK has continued to expand, reaching a new industry milestone for revenues as it surpassed £1b per annum. 475 new stores and 4.5m sq. ft. of additional self-storage were also created.

Overall, the average store size slightly decreased, which we attribute to the increased number of container sites as the average internal storage site is nearly 30,000 sq. ft. This year, self-storage operators have largely been able to increase the rack rate as consumers grow accustomed to price rises in a high-inflation environment, although occupancy has fallen. The industry added 8% of storage space and revenues grew by 9%, demonstrating that the majority of growth has been driven by increased supply. Affordability of rents has impacted both occupancy and churn rates, but demand is such that operators have generally replaced lower paying customers with new ones willing to pay a higher rate, albeit for shorter periods of time.

M&A market dynamics

While consolidation has continued within the self-storage industry, the market remains highly fragmented, with the ‘Big 6’ collectively holding 37% of the market.

Market leader Big Yellow increased its storage space by 200,000 sq. ft. last year, and raised £110m in October 2023 to support the build-out of 11 new stores and 2 replacement stores. Lok’nStore and Shurgard expanded their space by an additional 100,000 and 200,000 sq. ft. respectively, whilst Safestore and Access focused on their existing capacity. Storage King achieved the largest annual site growth by adding 300,000 sq. ft. to its portfolio.

In April, Shurgard announced a cash offer to acquire Lok’nStore for £378m with the deal expected to be approved by shareholders in June 2024 and completion scheduled for August 2024. The combined entity will become the third largest self-storage operator, with over 4.6m sq. ft. within the UK.

Publicly listed operators remain keen to deliver growth through acquisitions as well as new developments. Developing new sites remains necessary for operators due to the scarcity of high quality portfolios/sites coming to market. Valuation differences between vendors and acquirers have extended as a result of the increased cost of debt, lower commercial property yields and subduing investor sentiment.

The larger operators are still keen to acquire multi-site operators that can add instant impact to their existing operations with many looking to infill geographical gaps in their portfolio. As a result of consolidation there are few operators with 5-20 significant sites across the UK. Such portfolios should attract a strategic premium if they came to market given the increased scarcity of assets.

Privately held operators remain keen to expand through acquisition as they typically generate returns at a greater rate than developing new sites. New sites characteristically have multi-year cash burn profiles until the site reaches optimal occupancy levels. These acquirers are actively seeking good quality single site operators that will allow for geographic expansion across the UK.

Looking to the year ahead, a general election approaches and so does the possibility of a Labour government. This could mean potential changes to the UK tax regime and the view at PKF Smith Cooper is that Capital Gains Tax rates are only likely to increase in the future.

Demand-side

The UK experienced a relatively soft landing from recession, with a recovery in growth forecast for 2024 and expected to strengthen in 2025. Growth was 0.6% quarter on quarter in Q1:2024, marking a stronger-than-expected exit from the technical recession during the second half of 2023. Interest rates remain high, continuing to significantly impact the housing market and, by extension, demand for self-storage. Residential transactions from January to November 2023 were down 19% compared to the same period in 2022. The self storage sector is intrinsically linked to the property market, with 32% of people stating a reason related to moving house when asked why they were considering self-storage. Overall occupancy levels have fallen back to 78% from record highs of 83% in 2021, but it is worth noting that this is in the context of an additional 8m sq. ft. of storage space becoming available in the UK over the same time period.

Many operators responded to record occupancy levels by implementing dynamic pricing strategies that increase rental rates compared to 2022 and 2023. The net impact is that the overall revenues have increased despite lower occupancy, demonstrating that demand for self-storage remains buoyant.

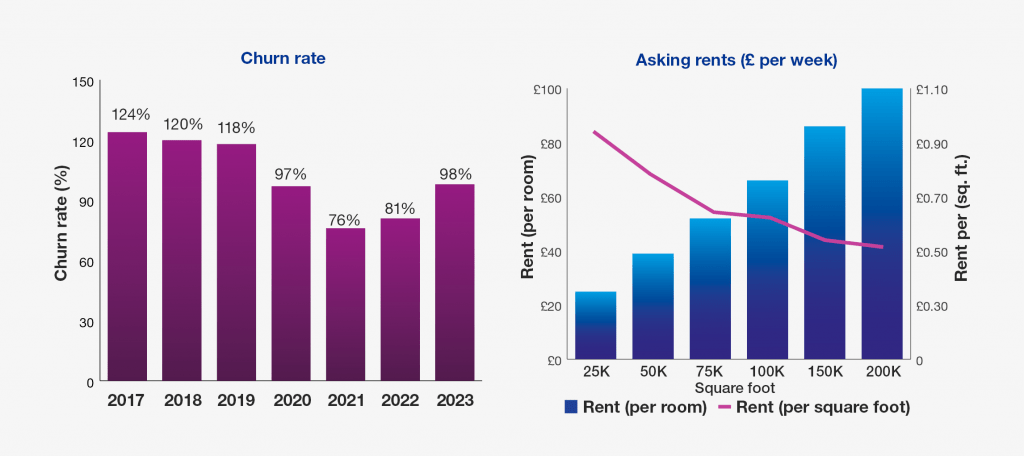

It remains important for operators to maximise returns by optimising each facility. The chart on the right displays the non-linear pricing structure that is typical in self-storage and shows how large units offer lower revenue per square foot than small units. However, there is customer demand for both small and large storage spaces, making unit mix a tough balancing act for operators as a facility with only small units would require more customers to reach the same occupancy levels as one with a mix.

While some operators continue to maintain the low churn associated with the pandemic era, in 2023 others have gone back to over 100%. Mature sites naturally experience lower churn, as older facilities tend to have more long-term customers. We understand customers are not staying as long, requiring facilities in their fill-up stage to attract even more customers to reach occupancy.

Supply side

2023 saw further expansion of the sector with 53 sites opening and the expansion of existing sites together adding an additional 4.5m sq. ft. of capacity to the industry.

There is a healthy pipeline of future developments, however planning permission is severely delaying progress and limiting space creation. Where sites are proposed in prime retail or commercial locations, the Local Planning Authorities (LPAs) take the view that sites provide lower employment opportunities than alternative uses. Established sites in such locations are therefore well sought after for acquirers.

Given the challenges in obtaining planning permission for new internal storage facilities, we are observing that volumes of smaller container-based storage facilities continue to rise. These facilities are typically smaller and located in out-of-town/rural areas with customers willing to travel further distances in order to take advantage of cheaper pricing and drive-up access to units.

Last year we commented on the emergence of remotely managed stores and now 13% of stores report no permanent staff member on-site. New technology solutions, such as Nokē Smart Entry Remote management, mean that remotely managed stores are not just reserved for smaller, regional stores but can also apply in prime locations.

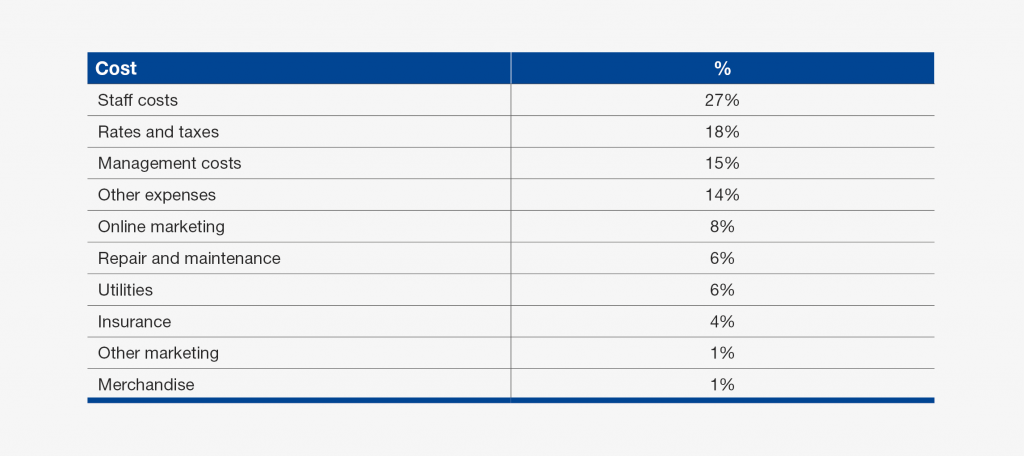

Self-storage benefits from a low cost base. Staff is the largest cost within the industry, as many operators employ one or two people per store. Cost inflation has not affected the industry as significantly as other sectors, however it has led to management costs increasing by 5% as third-party providers have raised their prices to counter-act the effects of inflation.

HMRC recently changed how they interpret mezzanine flooring in the context of plant and equipment, which has in turn affected its eligibility for capital allowance. The self-storage sector has now been impacted with one operator being refused their claim. For advice and support on capital allowances claims, contact the PKF Smith Cooper capital allowances specialists.

UK market in relation to the international market

The UK market dominates the European market in store count, owning a 32.9% market share of all stores across the continent. Within this share, there are 1500 internal stores with circa 800 container sites.

However, the UK market still has a long way to go to match the success of self-storage in the US. Savills notes that the US has 9.44 sq. ft. of self-storage per person. In comparison, the UK has just 0.73 sq. ft. and continental Europe a mere 0.21 sq. ft.

ESG

Sustainability continues to be a strategic priority across the self-storage industry. Many operators are actively exploring ways to improve the sustainability of their current business strategies.

70% of operators now use LED lighting, a 32% year-on-year increase. There has also been an increase in European operators employing passive infrared detection to limit energy waste. However, the uptake of more costly sustainability measures remains low, with solar panels utilised by only 7% of self-storage operators and electric vehicle charging points by only 5%. These features are more likely to be found in newly built facilities rather than in units where they have been retrospectively fitted. Uptake is likely to rise in the future though, as these installations become more cost-effective and through additional forthcoming regulatory pressures.

The additional interest in self-storage from private equity and real estate funds is likely to drive the ESG agenda, as these investors have to report on ESG criteria.

Future of the industry

The self-storage industry has already changed significantly over the past few years, with the adoption of new technology automating and digitising much of the sector. Looking ahead, self-storage will continue to evolve with key themes being:

1. ESG Investing in solar panels, passive infrared lighting sensors and other sustainability measures for facilities will not only see a positive impact on long-term profitability, it also keeps the pool of potential acquirers open.

2. Freehold v Leasehold PKF Smith Cooper is observing a shift back toward freehold sites. Owners and potential acquirers prefer freehold sites or at least long term (25+ year) leasehold properties. Leaseholds allow operators to enter the selfstorage industry with less capital. However, when it comes to acquirer appetite, many do have a preference for freehold over leasehold.

3. Security Break-ins and theft are on the rise, with 1 in 3 operators reporting a break-in last year. This is likely to rise given the prevalence of unmanned sites combined with deprioritised law enforcement. As a result, operators are beefing up deterrents such as active monitoring rather than relying on passive methods or CCTV.

4. Technology

a. Dynamic pricing – Automated systems that adjust unit prices in line with supply and demand are becoming more common. Dynamic pricing may maximise revenues, occupancy and profit.

b. Facewatch – Facial recognition systems have received sign-off from the Information Commissioner’s Office for compliance in proactive detection of suspect individuals. It is already being used by major retailers to identify potential shop lifters. The system has considerable potential within self-storage for customer identification and modernising access control, as well as identifying problem customers as soon as they enter a facility.

5. Pricing transparency – The government is in the process of drafting legislation to make headline prices more transparent. This may impact operators that advertise low cost initial deals to attract new customers. It may also affect operators that add mandatory fees for customers onto their unit rental prices, such as fob deposits or insurance. Securing new customers will likely become more challenging, especially taking into account current occupancy levels.[bg_faq_end]

PKF Corporate Finance specialise in providing advice to support clients on buying and selling businesses as well as accessing the debt and equity markets to support business growth. Through PKF International, we have boots on the ground in over 150 countries, meaning we are able to access international investors and acquirers. We deliver practical, commercially-viable advice with positivity and tenacity. We strive to deliver exceptional service, irrespective of deal size, by building close relationships with clients, keeping them well-informed and guiding them through complex transactions.

If you’d like further information regarding the contents of this document, or you’d like to find out more about how we can help you and your business, please get in touch.

Download publication