When you set out with the aspiration of selling your business, completion mechanisms are far from your mind, but understanding them and the impact on your net proceeds is a crucial part of the process, and of the work carried out by your corporate finance advisors.

What is a completion mechanism and why is it needed?

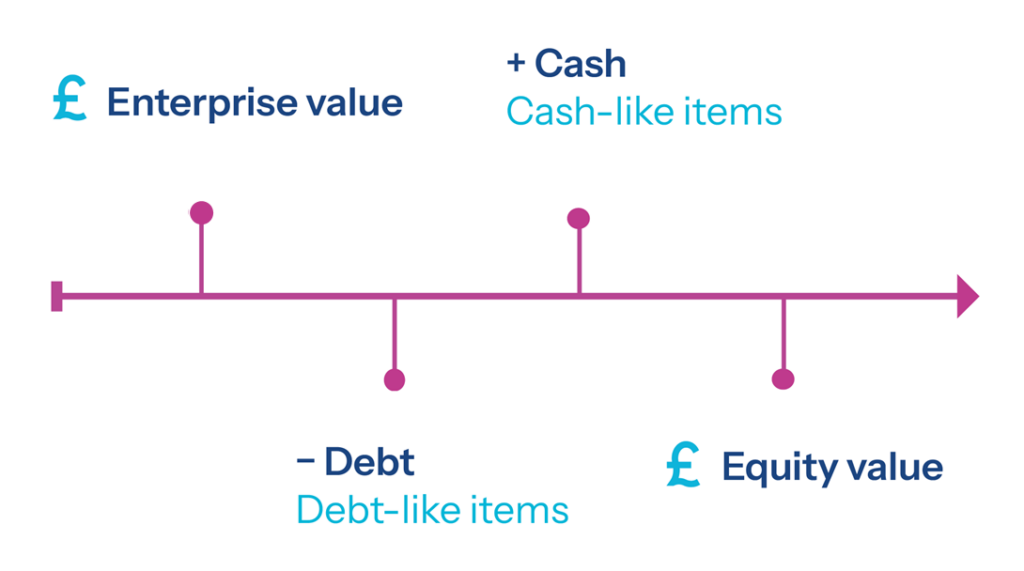

Usually, when you sell a company, you sell it for its ‘enterprise value’, being the market value of the company. This is then subject to adjustments such as additions for any cash or deductions for any debt, and subject to a normal level of working capital. This is very similar to the sale of a house where the ‘enterprise value’ of the property is its market value, and the equity value is what you receive after deduction of any debt against the property.

A completion mechanism is the calculation required to ensure that the equity value is calculated correctly. The rules tend to be based on ‘facts’ with a particular focus on the balance sheet and cash generation.

The completion mechanism is designed to calculate the correct amounts for cash, debt and working capital at the time of completion to ensure the correct equity value is paid for the business.

Cash-like and debt-like items

The simple illustration above does not necessarily account for all the potential adjustments to price. Cash and debt items may include the obvious: cash in any bank accounts, petty-cash, all third party debt and interest accruing on it. But we also need to consider items which are due to or from the company and not in the normal course of trading.

Examples of cash-like items can be:

- Rental deposits

- R&D tax claims receivable

- Other tax reliefs such as those that come as part of the exercise of an EMI scheme

- Value of tax losses, if they can be utilised post transaction

- In some cases, capital expenditure made for growth purposes and the cost of recent M&A.

Examples of debt-like items include:

- Corporation tax payable up to completion

- Related party loans

- Overdue tax liabilities (including PAYE and VAT).

Working capital

A buyer will expect a normal level of working capital to be left in the business at completion. Working capital typically includes stock, WIP, trade debtors, prepayments, trade creditors, accruals, provisions, PAYE, VAT, and any other current assets/liabilities which directly relate to day-to-day trading activity. Essentially, the items on the balance sheet that are not fixed assets, cash, debt or deferred tax.

To calculate the normal level of working capital of a business, the average of the last 12 months is often used (adjusted for any exceptional items). The period of review depends on the working capital cycle of the business and sometimes forecasts may be used, particularly if the business is in a growth phase.

Subjectivity

There are many items where classification as debt, cash or working capital is subjective. Some of these can be industry specific, so it is worth investing a little time in analysing your balance sheet to assess how your items are likely to be classified.

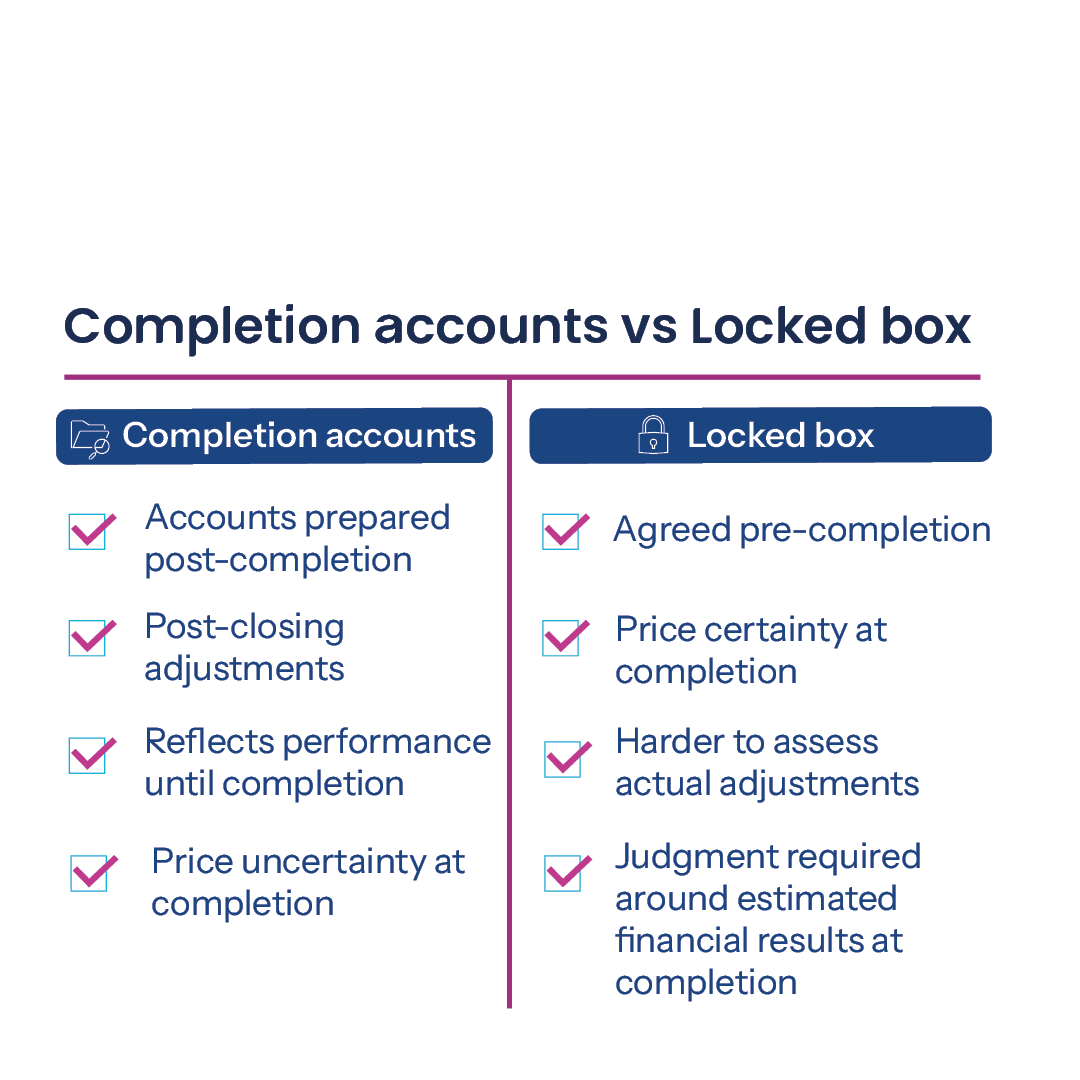

Locked box vs completion accounts

To evaluate the equity adjustments (cash, debt and working capital) there are two main types of completion mechanisms: locked box mechanism and completion accounts mechanism.

Completion accounts mechanism

Completion accounts are used to calculate the final equity value after the deal has actually completed based on actual results to the completion date, but subject to the agreement of specific accounting policies in the Share Purchase Agreement (“SPA”).

Normally, at completion, estimates of the key cash, debt and working capital items are used to estimate the equity value. The completion accounts are then used as a ‘true-up’ after completion when all the accounting information is available, ensuring all transactions are included.

Once finalised, completion accounts do give certainty as they are based on actual accounting information. However, they also leave the deal open to further negotiation and judgment of included items, making it crucial to clarify the specific accounting policies to avoid any disputes and the introduction of an independent expert to resolve. It also means that any final payment (buyer to seller or seller to buyer) is unlikely to be paid until a few months after completion.

Completion accounts are often seen as expensive to design due to the costs associated with drafting into the legal documents, producing the accounts and both sides reviewing them.

Locked box mechanism

Locked box accounts are designed to ensure that, at completion, the final equity value is known, the full price is paid and there is no further adjustment after the deal has happened.

Locked box accounts are prepared at an agreed point in time, referred to as the ‘locked box date’. This is usually a month-end date one to six months prior to completion where accounts are available. They can easily be diligenced by a buyer, which then gives certainty of the numbers to be included in the enterprise value to equity value bridge calculation.

When we ‘lock the box’ at an agreed date, the balance sheet amounts to be included as cash, cash-like, debt, debt-like and working capital items are fixed at that time. Adjustments are then required to account for the cash profits for the period up to completion and also for any ‘leakage’.

Leakage includes those amounts that are payable to the shareholders, or for the benefit of the shareholders, which are not permitted amounts. This can include dividends, personal payments, bonuses, transaction costs and more. If they are known before completion, they will be included in the enterprise to equity value bridge as debt-like items, and if they are not known at completion, the SPA will allow the buyer to claim for any amounts paid out during that period.

Permitted leakage refers to those items agreed as payable to the shareholders pre-completion, which normally would include salaries or management fees.

The calculation of profits can be based upon a profit ticker, which is an equal amount of cash profit estimated by the advisors and multiplied by the number of days from the locked box date to completion. Sometimes an interest rate is used, but this is quite subjective. Alternatively, an estimate of the actual cash profit, based upon management accounts or other financial information, is calculated.

Ultimately, the purpose of all the above analysis is to ensure that a fair equity value for both the buyer and the seller is calculated. That value is then paid at completion (subject to any deferred consideration). The amount of analysis required is high; there are often many points to negotiate, but all with a view to protecting value for all parties.

Final equity value: the importance of seeking professional advice

Determining the final equity value in a business transaction is a highly complex process, which requires a deep understanding of concepts such as enterprise value, equity value, cash-like and debt-like items, and working capital adjustments. Each transaction may involve unique factors and specific tax treatments, all of which may impact the final outcome.

Given the technical nature of these assessments and the potential for significant financial consequences, it is essential for both buyers and sellers to seek professional advice. Experienced corporate finance advisors can help navigate the complexities, ensure that all relevant factors are considered and protect value for all parties involved.

If you are considering selling your business, contact PKF Smith Cooper to arrange a call with one of our corporate finance experts. We can guide you through the process from start to finish and help you to determine which completion mechanism is most suited to your business needs and objectives.